The OECD has recently released information on the two most important recent global networks of global tax information exchange. They are, respectively, the networks of exchange of country-by-country reporting (CBCR) and exchange of financial account information (through the Common Reporting Standard, CRS).

These networks give a unique look into the new political economy and geography of global tax information flows. CBCR and CRS data are, arguably, the cornerstones of modern global tax information cooperation, providing crucial data on the foreign activities of national individuals and companies. The CBCR is an annual report for large multinational groups (revenue +€750m) that states their jurisdictions of operation, the nature of business in each country, the tax paid along with a host of economic activity indicators. The CBCR is typically filed in the corporate headquarter’s country of residence, then shared on request with other countries as needed. Through the CRS, each government compiles data from national banks on the financial accounts (balances, interest, dividends, and financial asset sales proceeds) of non-citizens, which is then exchanged automatically with those citizens’ home competent authorities.

Therefore, it is also highly interesting to look at the global network of these information flows – who has access, who doesn’t, and who is connected.

So I scraped the data off the OECD website and analysed it. And what I found provides a very interesting picture of the modern tax information networks.

At the time of writing, there were around 700 (CBCR) and 1600 (CRS) bilateral exchange agreements established. (I’m not sure why OECD say 1800 CRS agreements because there’s only 1600 unique agreements in their data). Given that the CRS was launched four years ago and CBCR only two, the discrepancy is natural. Taken together, the 2300+ agreements are a quite fascinating data set. Let’s look at each in turn, and then the two together.

First, however, a key caution must be noted. While the CBCR and CRS provide key recent mechanisms of tax information exchange, they are by no means the only mechanisms. Preceeding the new CBCR and CRS networks are established networks of bilateral “by request” exchange of information networks (the previous OECD standard), bilateral tax information exchange agreements (TIEAs) and tax treaties with info exchange clauses. Given that these have been in place for much longer, they are naturally more dense than the new networks. Still, CBCR and CRS are the frontier and are replacing these older standards exactly because of their limitations. Thus, the analysis below provides a picture of the emerging state-of-the-art within global tax information exchange.

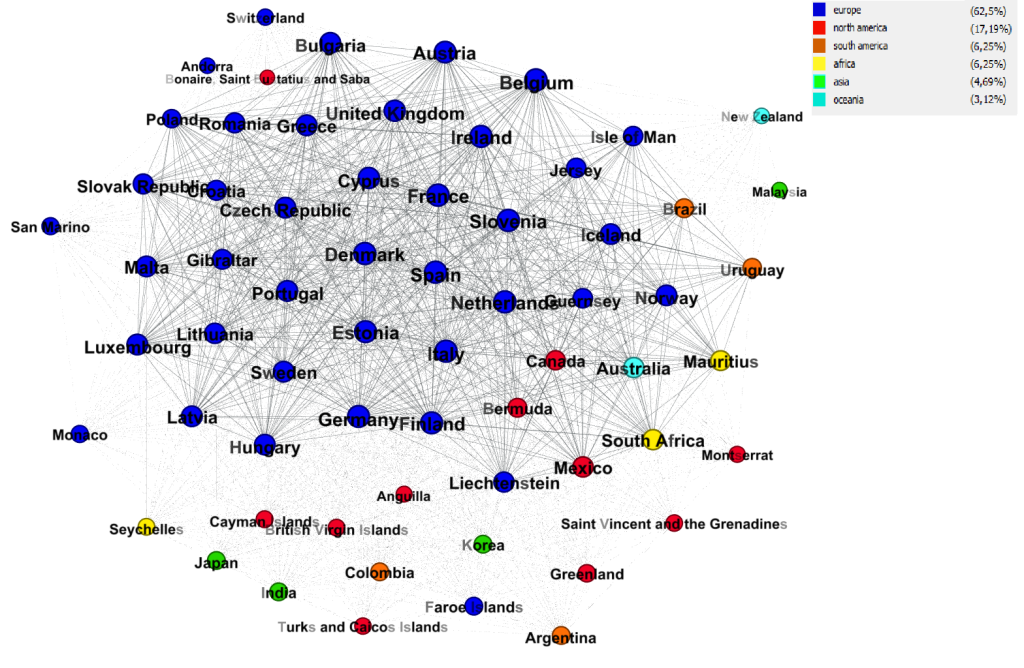

The global CBCR exchange network

I tweeted out the network the other day, and it looks like this:

(Size by degree (number of links); node colour by region; and network layout by ‘ForceAtlas2‘.)

There are a few caveats to be noted before drawing lessons from this picture. First, the novelty of CBCR shapes the network look substantially. The picture is dominated by European countries, but that is understandable given 55% of all CBCR exchange agreements are formalised by EU Directive 2016/881/EU on automatic exchange of tax information (the rest are individually negotiated CBCR MCAAs). Second, the absence of the USA is noteworthy. While the USA has been reluctant to commit to reciprocal information exchange of bank account data, that is not the cause for CBCR. Simply, US CBCR filing requirements will kick in on 31 December 2017, as in most jurisdictions, but later. It is almost assured that the US will develop an extensive exchange network to protect US MNEs from local filing demands. Other countries with late filing requirements that will be expected to build substantial exchange networks as we go include Hong Kong, Japan, Russia and Switzerland. The whole network is expected to increase substantially over the next few years, as the remaining CBCR MCAA signatories (as of today, there were 57) conclude and report agreements.

That said, what we can see is that the current global CBCR network is all about Europe, OECD members, and a few small offshore centres. That picture likely won’t change too much. The almost complete absence of South America (beyond Brazil and Uruguay), Asia (beyond Malaysia), and Africa (beyond South Africa and Mauritius) stands out. This has attracted renewed criticism that the OECD tax policy-making processes are not inclusive of developing countries. However, it should be noted that the OECD has moved in the direction of bringing developing countries more closely in to its tax work, including through the BEPS Inclusive Framework, so there is potential for a broadening of the geographical concentration in the CBCR exchange network.

It is also worth noting that the picture indicates a very clear “you’re either in or you’re out” trend. There are currently 45 countries exchanging CBCR data, and none of these have less than 23 agreements (maximum of 43). If you are set up to exchange CBCR data, you are ready to exchange it with many partners.

More broadly, I think the network shows quite nicely the varying allegiance to the OECD international tax consensus. The European Union, in particular the European Commission, has become an increasingly autonomous player in international tax affairs but also a close ally of the OECD on many counts. The centrality of Europe in the global CBCR network is a representation of this position.

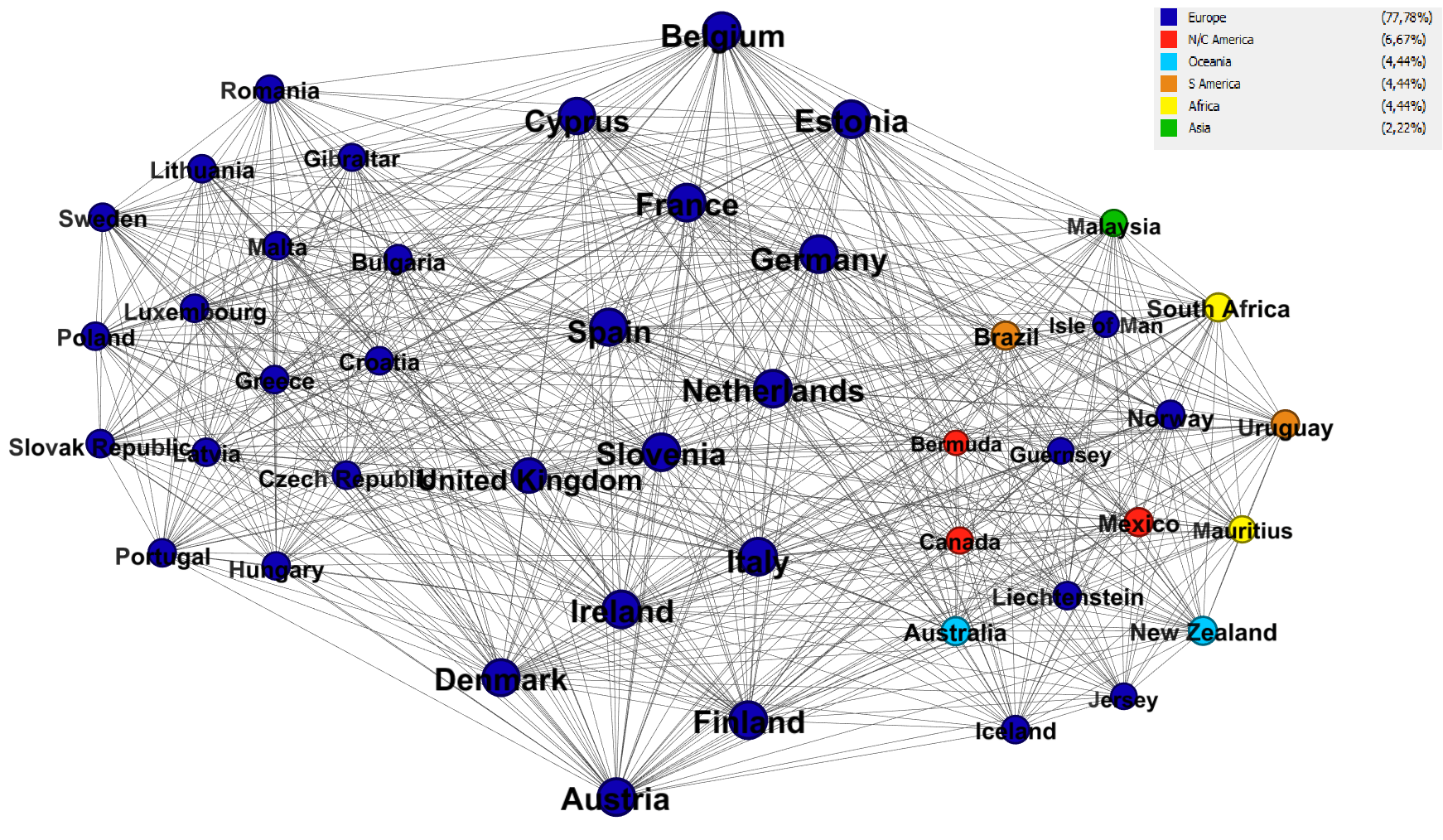

The global CRS exchange network

(Again, size by degree (number of links); node colour by region; and network layout by ‘ForceAtlas2‘.)

The global CRS network provides a somewhat more developed but not substantially different picture of the new political economy and geography of global tax information exchange. The fact that we have 62 countries (as opposed to 45) and more than twice the number of exchange agreements makes for a more pronounced illustration.

Again, it is worth noting some points on the data. Once more, EU is massively present. This is partly because of its speed in implementing effective CRS legislation. Thus, 35% of CRS exchange relation are down to EU instruments, including EU Directive 2014/107/EU. However, EU members have also been active in concluding agreements with non-EU members. The remaining 65% of exchange relations are concluded as individually negotiated CRS MCAAs, plus ten exchange agreements through the UK CDOT (Crown Dependencies and Overseas Territories International Tax Compliance Regulations). We can also see that, again, the US is absent. However, here we should not expect it to develop a network at a later stage. Due to the presence of FATCA, the US’ own financial account information standard, there has been no desire to also sign up to the CRS. Finally, the CRS network is also expected to increase and broaden its geographical scope over the coming years as the remaining of the AEOI-committed countries (100 at the time of writing) conclude and report on exchange agreements.

Beyond that, the political geography of the CRS network is notably similar to that of the CBCR network: It’s all about Europe and OECD members, with a few small offshore centres mixed in. Like the CBCR network, the absence of developing states has also contributed to criticism of the CRS standard. Once again, we can also see that it’s very much an “you’re in or you’re out” picture. 62 countries have CRS exchange agreements, and only one (Bonaire, Saint Eustatius and Saba) has less than 29 agreements in place.

Another nugget that I found quite interesting in the data: There are around 350 CRS agreements that are only reported by one of the two jurisdictions to the OECD. All other relationships are reported by both jurisdictions. For instance, Anguilla’s CRS exchange agreement with Argentina is only reported to the OECD by Anguilla, not Argentina. And there is a certain trend with these 350 agreements. They are all reported by the following countries: Anguilla, Bermuda, British Virgin Islands, Cayman Islands, Croatia, Cyprus, Korea, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Mauritius, Mexico, Monaco, Montserrat, Netherlands, Romania, Saint Vincent and the Grenadines, Turks and Caicos Islands. Most of these countries are small (island) states with noteworthy financial centres, or what some might label tax havens.

There are a few possible explanations, but my guess as to what is going on here is this: Countries most at risk of reputational damage and political wrath from non-compliance are making sure they report all of their exchange relations to the OECD as soon as possible. They simply want to make sure it is noticed when they are conforming to expectations, when they are “doing good”.

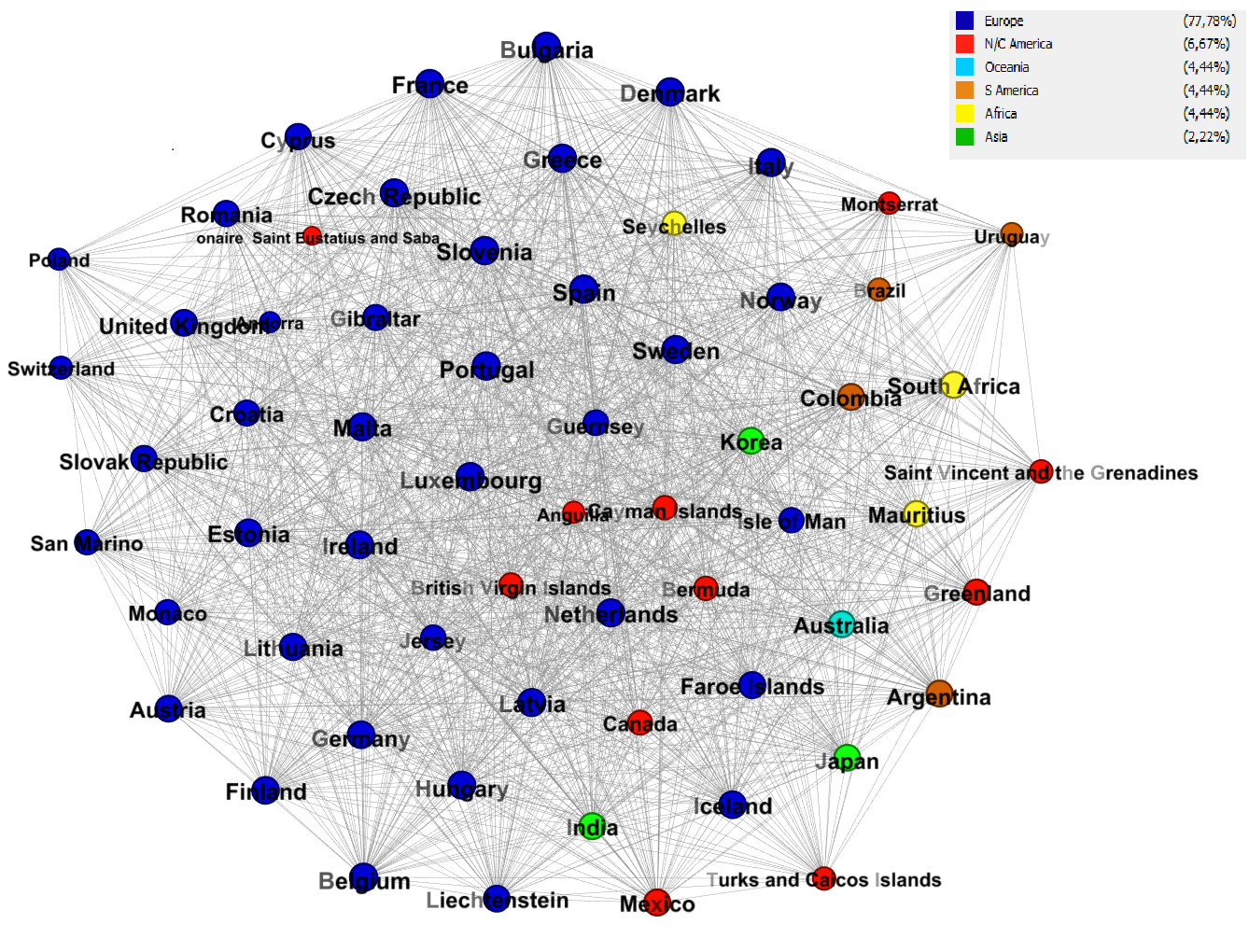

The global tax information exchange network (CBCR + CRS)

(Size by weighted degree (number of links, weighted by strength); node colour by region; and network layout by ‘ForceAtlas2‘.)

Here, I’ve added the CBCR and CRS relationships together, giving us a picture of who is truly able to access modern global tax information flows. The bolder the link, the more weight it has, indicating access to both CRS and CBCR information from international exchange.

Having noted caveats to the data above, the picture that emerges here is, as we might have expected, more pronounced but similarly indicative as the individual CBCR and CRS networks. The observations barely need repeating, but for good measure: there’s EU/OECD dominance with a few financial centres mixed in, an absence of the US and developing countries, and a strong in-or-out dynamic.

Given the current structural factors contributing to this network layout, the main factor with potential to substantially change this picture is change in the overall political economy of global tax governance. This may yet happen, e.g. through the BEPS Inclusive Framework, but may also very well not happen due to geopolitics or other factors.

There will be more analysis to do on this data, and it will be interesting to follow the longitudinal development of these networks. I will certainly continue my work in this area, as I’m sure others will. For now, however, a very interesting picture is emerging of the new political economy and geography of global tax information exchange.