-

The Paradise Papers should lead us towards a new global tax system

Last week, I published an op-ed in Danish newspaper Politiken with my colleague Saila Stausholm. I reproduce it below, liberally translated, for those interested. Given the op-ed format, it naturally has certain limitations and a certain style that differs from my usual writings on this blog – so take that into account. Here we go: The Paradise…

-

Varieties of Something

What is a tax haven really (if anything at all)? How can we classify them? And what are the existing attempts at doing so? In connection with a research project, I recently asked for your help in pointing out sources discussing different “varieties” of tax havens, i.e. what different countries “specialise” in. That fostered a series…

-

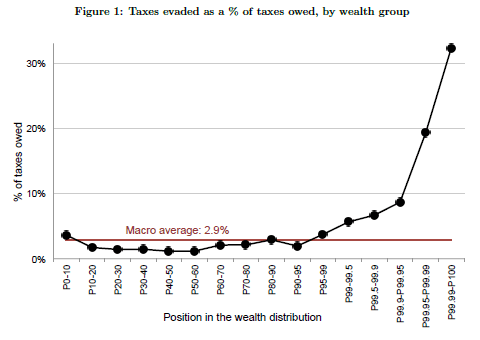

Why do people evade taxes?

-

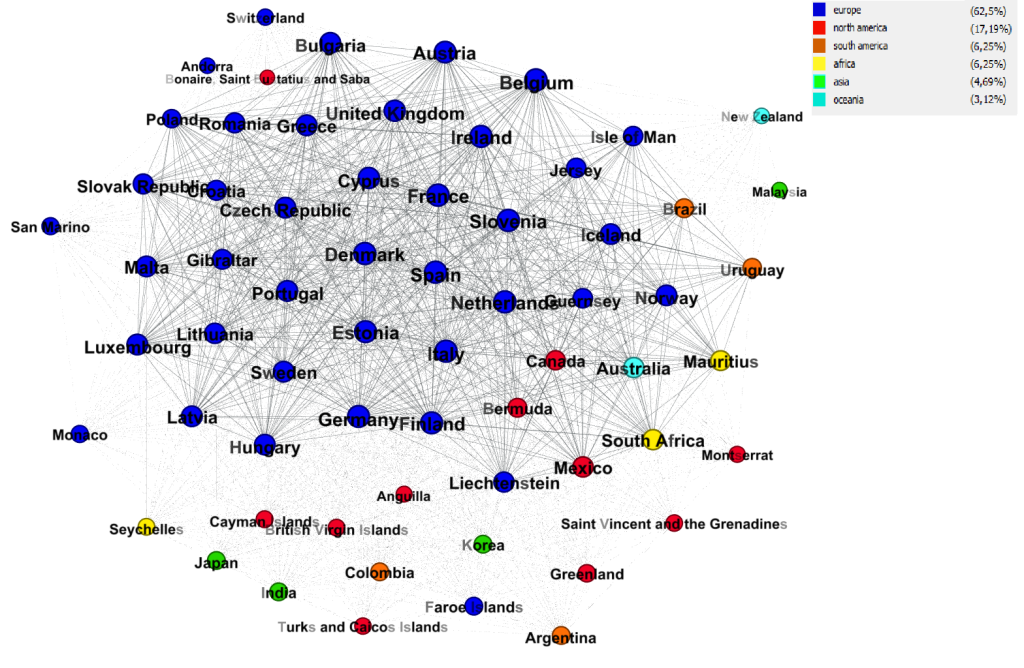

The new political economy and geography of global tax information exchange

The OECD has recently released information on the two most important recent global networks of global tax information exchange. They are, respectively, the networks of exchange of country-by-country reporting (CBCR) and exchange of financial account information (through the Common Reporting Standard, CRS). These networks give a unique look into the new political economy and geography of…

-

The bark IS the bite, but ..: Why tax haven blacklists are not the answer

The OECD has been working on criteria for a tax haven blacklist. At the request of the G20 Finance Ministers, this has been a work in progress since April of this year. And the results are set to be presented at the G20 finance minister’s meeting in China next month. This morning, the FT reports that…

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.