A much talked-about recent paper by economists Annette Alstadsæter, Niels Johannesen and Gabriel Zucman has re-ignited popular attention to tax evasion and inequality.

While discussion of reliability and methodology have prevailed in some corners of social media, the broader questions raised by the fascinating new study should remain at the fore: Why do people evade taxes? Who evades taxes? How can they do so? And what are the effects – on our societies, institutions, political systems, and so forth?

In this post, I will look at what the existing academic literature has to offer on these questions related to tax evasion, in particular the former: Why do people evade taxes? And I’ll zoom in on how recent contributions, such as that by Alstadsæter et al. and others, adds to this scholarship.

What shapes tax compliance?

Existing work on tax compliance is abundant, in particular within behavioural economics, sociology and psychology (see reading list at the bottom of the post). This scholarship has highlighted five central factors that particularly shape tax compliance in the national context:

- Levels of wealth

- Tax rates

- Audit probability and penalty

- Tax morale

- Institutional environment

Firstly, wealth typically enhances the probability of tax evasion. Wealthy people simply have more ability to evade. They have more and more flexible sources of income, allowing for manipulating and escaping of national regulatory and administrative powers. Think of the Ultra-High Net Worth Individual (UHNWI), who can offshore his financial assets and the accruing gains or move artworks stealthily across the globe – as opposed to the carpenter or teacher, whose main income (salary) is typically taxed at source.

Second, relatively higher tax rates foster relatively more evasion. Because taxes are often perceived as an undue burden (rightly or wrongly), the willingness to evade rises with the tax burden. As I have written elsewhere, this is extensively discussed in the economic literature. Even though taxes also pay for public spending (the fiscal coin), there may be a reasonable expectation by wealthy taxpayers that any evasion on their part will not lead to a deterioration in public spending in relation to the public goods from which they benefit, or that the benefit received from corresponding taxes simply does not provide sufficient value.

However, it is worth noting that it is mostly large differences in tax rates, and at the margins, that foster tax evasion. As an indicator, a number of experimental studies have found that increasing tax rates e.g. from 30% to 50% had little or no effect on compliance, whereas raising from 5% to 25% or from 5% to 60% does have an effect. Related, recent economic modelling on optimal corporate tax rates also suggest that only very high tax rates inhibit growth.

Third, potential tax evaders assess the risk of getting caught through audit probability and penalties/punishment, adjusting their behaviour accordingly. If a taxpayer perceives a high risk of being audited (and thus caught) and/or a substantial penalty (economic or personal), they are simply less likely to engage in tax evasion. This is as much about the perception of audit risk and penalties (which can be fostered in various ways) as it is about the actual probability of audit and penalty.

Fourth, the individual taxpayer’s tax morale is a decisive factor in tax compliance. Tax morale encompasses the social and cultural norms, and individual allegiance hereto, shaping compliance motivation. Tax morale itself is a highly complex phenomenon, dependent on a host of factors. The ‘morale fibre’ of each individual – the dispositions one is ingrained with given a life history of events and perceptions – is obviously instrumental. The extent to which people perceive taxes as part of a valuable quid-pro-quo is also central. As noted above, when the cost of taxation is viewed as too high compared to the benefits received, people are more likely to engage in evasion. Finally, the social environment matters: where people trust each other and perceive high tax morale in each other, it will deter evasion.

Fifth, the institutional environment determines the taxpayers’ willingness and ability to comply. Formal (such as political organisations) and informal (cultural ‘rules of the game’) institutions associated with the tax system shape tax compliance. On the former, trust in public institutions is a well-known determinant of taxpayers’ willingness to pay; if we trust our democracy, if we perceive the tax system as fair, if we believe the political system is efficient, we are more likely to pay our taxes. This is why revelations of corruption or scandal are likely to negatively affect tax morale. For instance, in the Danish context, recent revelations of massive dividend withholding tax fraud have been found to harm societal tax morale. On the latter, socio-economic and psychological factors can help explain tax morale, such as interpersonal trust and belief in fiscal cost-benefits.

Recent contributions 1: Tax evasion and inequality

Now let’s circle back to the first paragraph of this post: the new Alstadsæter-Johannesen-Zucman paper. This is a contribution mainly to point 1 above, i.e. levels of wealth as a determinant of tax evasion. But it also raises questions more broadly about the structure of evasion and the effects on our societies. There have been plenty of media stories about the paper, so let me just highlight three particularly relevant contributions in the context here:

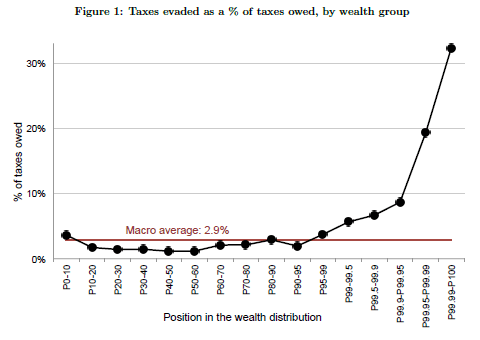

First, the AJZ paper illustrates the progressiveness of tax evasion by wealth more clearly than perhaps any paper before it. Using data from the HSBC SwissLeaks, Panama Papers, Swedish and Norwegian tax amnesties, as well as data from the Scandinavian tax administrations, they show a remarkably clear trend of increasing probability of hidden funds (which are likely to correlate with evasion, although this is an assumption up for challenge) with wealth. It indicates that it is the utmost wealthy, in particular the top 0.01% (owning more than $40m in assets), that evade taxes via offshore structures (which is likely to cover a similarly increasing proportion of evasion mechanisms by wealth due to fluidity of income and assets, as noted above).

Second, the paper indicates that tax amnesties may be a more effective tool to combat tax evasion than previously thought. While tax amnesties are typically criticised for merely offering a one-time free lunch to wealthy tax evaders, the study finds that tax amnesties in Sweden and Norway have had positive, lasting effect on tax payments, and reported wealth and income, by taxpayers using the amnesty. However, it is important to caution the interpretation with some key points. Firstly, the data utilised here relates largely to the mid-2000s, where we did not have FATCA, the CRS, or today’s levels of international tax administration cooperation. The presence of new modes of information exchange are likely to squeeze scope for tax evasion (and avoidance) by wealthy taxpayers, thus potentially eroding the benefits of tax amnesties. More broadly, while tax amnesties may have a positive effect on the tax compliance of individuals with a history of evasion, we know little about its societal effects. From the literature reviewed above, we might hypothesise that the presence of amnesties deteriorates trust in political institutions, belief in a fair tax system, and perceptions that others are compliant – all of which would decrease societal tax morale.

Third, AJZ touch upon the implications of their findings, in particular as it relates to inequality. Ever since Piketty, inequality has been at the top of national and global political agendas. This paper, alongside other work by the authors (and others), shows that unrecorded offshore wealth substantially skews national inequality and tax burdens, leaving national statistics incomplete. The paper estimates that the top 0.01% hide about 25% of their true wealth, and that counting hidden offshore wealth increases the wealth share of Norway’s top 0.1% from 8% to 10%. You can easily imagine what this does to national (and global) inequality statistics. Given that tax compliance is generally higher in Scandinavia than anywhere else, it is likely that the inequality skew shown from Scandinavian data provides a lower bound for the rest of the world.

Recent contributions 2: Comparative experiments in tax compliance

Another stream of scholarship that has contributed important recent insights is comparative experimental work on tax compliance. This scholarship provides insights mainly for points 4 and 5 above, i.e. tax morale and institutional contexts of tax compliance. Here I’ll highlight recent work by a group of mainly Italian-based scholars, with two recent pieces (1, 2), though I must also mention that my colleague at Copenhagen Business School, Alice Guerra, has embarked on a fascinating 2-year post-doc project to build on and strengthen this line of work. Using controlled experiments involving Italians, Swedes and Britons, the Italian-based scholars are able to gauge differences in tax compliance and its sources across national contexts. Here I’ll highlight two particularly relevant contributions for this context:

First, while Italians (and Southern Europeans more generally) are typically viewed as having low tax morale compared to Britain (Northern Europe) and in particular Sweden (Scandinavia), the studies in fact showed surprisingly little variation in the intrinsic motivation of subjects to comply, when facing similar circumstances. In fact, Italians were even showed to have higher propensity for tax compliance than Britons given identical institutional environments (simulated in the experiments). This is despite consistent measures of relatively lower trust and honesty (factors that we would think lead to higher evasion) in Italy, and a general perception of Italians as less moral. This indicates that it is not, as conventional wisdom holds, the lack of intrinsic motivation on the part of Italians that hinders tax compliance.

Second, the national “style” of evasion is important in determining tax compliance. While Swedes for instance are more likely to comply in full than Italians, they are also more likely to not comply at all. It seems that in Sweden, there is a “either or” dynamic to tax evasion. In Italy, in contrast, there is a much more significant propensity to fudge (i.e. “cheat by a small amount”). Although the overall effect is that Swedes and Italians’ tax morale is relatively similar, the structure of national tax morale varies significantly.

Policy implications

While these studies and all of their contributions are valuable in themselves, enhancing our understanding of tax compliance and evasion, we would be foolish not to look at potential policy implications. I would not recommend full regulatory overhauls based on individual studies, but taken in context of wider bodies of literature, we can sketch out some preliminary lessons.

From the tax evasion and inequality literature, it is clear that tax administrations and legislators must pay particularly close attention to evasion by wealthy people, designing and implementing targeted policies to combat offshore evasion. This realisation has not been lost; it is behind much of recent years’ surge for automatic exchange of information and tax transparency at the global levels. The emergence of FATCA and CRS, while shortcomings remain, are likely to make a substantial impact on offshore tax evasion by wealthy individuals, deterring some avenues of evasion whilst channelling illegal activity toward other vehicles (such as trusts), where new regulatory innovation must then focus accordingly.

It also points to tax amnesties as a potentially useful tool to instil lasting tax compliance in prior evaders. However, this must be balanced against any deterioration in wider societal tax morale due to perceptions of injustice. Perhaps a useful approach would be to utilise the revenue brought in from tax amnesties specifically to raise societal tax morale, such as via broad-based campaigns or strengthening the integrity of public institutions.

Finally, there is a need to recognise shortcomings in national wealth and inequality statistics. Putting offshore wealth in the spotlight provides an opportunity to gain a more real picture of inequality and wealth in national and international contexts, which should be to the benefit of polities and citizens alike – no one is better off with continuing concealment of actual wealth distributions, except for tax evaders.

Based on the experimental tax compliance literature, we would do well to start questioning prevalent narratives of a “moral North” and an “amoral South”, certainly as it relates to tax compliance. Italians are no less willing to pay taxes than Britons or Swedes.

Rather, recent studies tell us that we should focus on the institutional context in which tax compliance happens. There is no denying that tax evasion is more widespread in Southern Europe than in Northern Europe, but the literature indicates this is not due to varying individual intrinsic motivation. Instead, there is a need for policy-makers to focus on implementing policies that eliminate formal opportunities for evasion. As an example, 95.9% of Danish personal income taxes are levied based on third party reporting (from banks, employers, unions, etc.). This makes it difficult to evade taxes. Similarly, the development of expansive networks of automatic exchange of tax information is likely to contribute to this end.

Finally, we must recognise the differing national “styles” of tax evasion. For instance, given that tax evasion for Swedes is very much an “either or” question, there is a need to focus deterring efforts on the initial decision to evade or not, as compared to Italy where focus should rather be on the culture of “fudging” (‘cheating a little bit’). This may foster differing policy initiatives that emphasise intensive and extensive decisions to evade taxes, respectively.

As a very last note, I must also emphasise that, although tax evasion is certainly a serious problem in many countries, North and South, as evidenced by the literature reviewed here, all the studies discussed here found that most people are honest and want to pay their taxes correctly. While Alstadsæter, Johannesen and Zucman estimate that many of the wealthiest taxpayers hide substantial fortunes offshore, most taxpayers clearly did not. The cross-cultural experiments also found that the vast majority of people genuinely do not look to evade taxes, (almost) no matter the circumstances. This is a lesson not to be forgotten.

Reading list on tax compliance

Alm & McKee, 1998. Extending the Lessons of Laboratory Experiments on Tax Compliance to Managerial and Decision Economics. Managerial and Decision Economics, 19(4/5): 259-275. Link.

Cullis, Jones & Savoia, 2012. Social norms and tax compliance: Framing the decision to pay tax. The Journal of Socio-Economics, 41(2): 159-168. Link.

Cummings, Martinez-Vazquez, McKee & Torgler, 2009. Tax morale affects tax compliance: Evidence from surveys and an artefactual field experiment. Journal of Economic Behavior & Organization, 70(3): 447–457. Link.

Fonseca & Myles, 2012. A survey of experiments on tax compliance. HMRC Research Report 198. Link.

Hashimzade, Myles & Tran-Nam, 2013. Applications of behavioural economics to tax evasion. Journal of Economic Surveys, 27: 941–977. Link.

Onu & Oats, 2016. ‘Paying Tax Is Part of Life’: Social Norms and Social Influence in Tax Communications. Journal of Economic Behavior & Organization, 124: 29–42. Link.

Pickhardt & Prinz, 2014. Behavioral dynamics of tax evasion – A survey. Journal of Economic Psychology, 40: 1–19. Link.

Torgler, 2002. Speaking to Theorists and Searching for Facts: Tax Morale and Tax Compliance in Experiments. Journal of Economic Surveys, 16(5): 657-83. Link.

Torgler & Schneider, 2007. What Shapes Attitudes Toward Paying Taxes? Evidence from Multicultural European Countries. Social Science Quarterly, 88(2): 443–470. Link.

One response to “Why do people evade taxes?”

[…] progressive (the richer, the more opportunity), as illustrated by recent research. As I have also written previously, the legal and institutional framework is the key element in determining whether people comply with […]