Within tax economics, one of the central arguments for tax competition and low(er) taxes on capital, including corporate profits, is that it leads to increased investment and growth (at least in some countries, mostly small open economies).

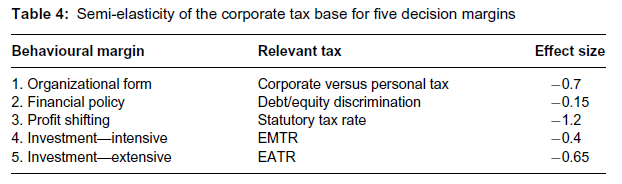

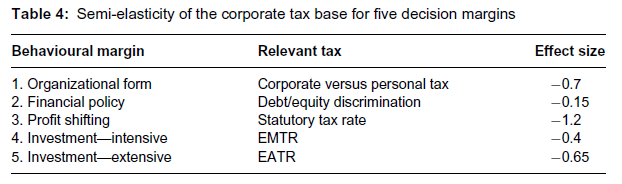

Why? In short, we know that corporate tax rates and rate changes have behavioural effects. Capital income may change legal forms (between two corporate forms or between corporate and non-corporate forms), firms may change their debt/equity ratios, they may shift profits abroad or increase/reduce investments. It is the nature and size of these effects that determine the result of corporate tax increases or decreases. The ‘go to’ for empirical evidence on this is De Mooij & Ederveen’s 2008 “reader’s guide”. Their literature review finds that, in an average situation surveyed by the literature, the total semi-elasticity of the corporate tax base for these effects (i.e. the % change in the tax base from a 1% increase in the relevant tax, see below) is -3.1, with profit shifting (-1.2) the largest single effect:

I.e. if the statutory corporate tax rate increases by 1%, the corporate tax base is predicted to shrink by 1.2% from increased profit shifting.

There are a myriad of potential arguments to question the certainty and applicability of these findings, but that is for another potential blog; suffice to note here that these figures represent the most accepted available evidence in economic literature on the behavioural effects of corporate taxation.

Based on this evidence, it is regularly argued that corporate tax rate reductions in isolation and tax competition more broadly positively support economic growth as facilitators of investment and eliminators of tax avoidance (again, in some countries at least).

Now, a key element in such assertions is that the status quo is taken for granted. Current behavioural effects (tax elasticities) are assumed as universally true. Rather than endogenous to economic tax competition models (i.e. “they can be changed”), behavioural effects are treated as exogenous (i.e. “this is how the world is”). As my review of Peter Dietsch’s recent book on tax competition notes:

One of the key points in Dietsch’s dismissal of tax cooperation as economically inefficient concerns optimal tax theory. Proponents of tax competition that leverage optimal tax theory hold that lowering taxes will result in increased labour supply and decrease tax evasion and avoidance. Analytically, the consequence is less need for tax cooperation to stem a race to the bottom of capital taxation. And this may be empirically true today. But these elasticies (the extent to which the labour supply and evasion/avoidance change with tax rate changes) are (partly) institutionally determined, and thus Dietsch argues there is no reason to assume today’s elasticities for tomorrow – they can be modified through policies and thus we can change the factors in the optimal tax calculation. For instance, by introducing stronger international cooperation on capital tax evasion, it is possible limit the tax evasion elasticity, and thus make tax systems more progressive by increasing the optimal levels of capital taxation, shifting the tax burden back on to mobile capital factors.”

The highlighted part is, in fact, exactly what is happening today and what has been happening for the past decade in particular. We’re changing the equation of tax competition and corporate profit shifting. Numerous and continuous reforms to combat tax evasion and avoidance are contributing to this evolution (even if some commentators questions their effectiveness). This includes regulatory initiatives (such as (automatic) exchange of information, FATCA and the CRS, the OECD MCAA, the revised EU Parent Subsidiary and Savings Tax Directives, the OECD Harmful Tax Campaign, Dodd-Frank, country-by-country reporting, the BEPS project, the EU ATAD and the EU tax state aid investigations) and voluntary standards (EITI, PWYP and the Fair Tax Mark), but also other significant developments (such as the Offshore Leaks, LuxLeaks and PanamaPaper).

Not just in their material effect but also in their normative impact do these reforms and events lessen the ability and willingness of corporations to shift profits as part of tax and regulatory arbitrage, thus decreasing the predicted elasticities (i.e. the positive corporate tax base effect from decreased corporate tax rates). This is not an unreasonable assumption, in any case. To my knowledge, there is still no systematic studies of the effects of these regulatory and normative changes on corporate tax elasticities.

This realization is what led Pascal Saint-Amans, Director of the OECD Centre for Tax Policy and Administration, to make the following comments in to the Wall Street Journal this week:

“For the past 30 years we’ve been saying don’t try to tax capital more because you’ll lose it, you’ll lose investment. Well this argument is dead, so it’s worth revisiting the whole story,” Pascal Saint-Amans, the OECD’s tax chief, said in an interview.

“In the past people, notably with international income, could use foreign bank accounts to receive and make payments and their home tax office would never know. That era will be over,” Mr. Saint-Amans said optimistically. “In the lead up to this new regime some countries have allowed their citizens to declare their foreign income without penalty, that alone has raised 50 billion euros in extra tax.”

Saint-Amans’ comments also come on the back of the OECD’s release of a new report entitled “Tax Design for Inclusive Growth“, which, as a lead up to this weekend’s G20 Finance Ministers meeting in China, breaks with the advice of prior decades, arguing that the case for low capital taxation and tax competition are “not as clear-cut as previously thought” (p. 40). Although this specific messaging was not included in the G20 meeting communique, the report’s section on capital income taxation is highly recommendable for those interested, and there is no understating the language used here and its policy implications.

The OECD is sending a message, which is likely to become increasingly prevalent: As reforms squeeze regulatory room for and normative consequences of tax competition, capital is less likely to flee national boundaries, and thus countries can, just perhaps, slowly start to ease the foot off the tax competition throttle.

* POST-SCRIPT JUNE 2018 *: A new paper by the IMF was released on this exact topic recently. I shared some thoughts on the paper on Twitter, which provides a relevant addendum to this blog post. To read, see below:

4 responses to “We’re changing the equation of tax competition and corporate profit shifting”

[…] the other hand, and as noted elsewhere, over the past decades regulatory tightening of corporate profit shifting may have contributed to a […]

[…] tax administration cooperation. The presence of new modes of information exchange are likely to squeeze scope for tax evasion (and avoidance) by wealthy taxpayers, thus potentially eroding the benefits of tax amnesties. More broadly, while […]

[…] tax cuts: why the old analyses don’t stack up any more (did they ever?), which drew from another blog post by Rasmus Corlin Christensen. At the heart of this discussion is a long-standing dilemma: can the […]

[…] tax cuts: why the old analyses don’t stack up any more (did they ever?), which drew from another blog post by Rasmus Corlin Christensen. At the heart of this discussion is a long-standing dilemma: can the […]