-

Have we solved tax competition?

-

The Paradise Papers should lead us towards a new global tax system

Last week, I published an op-ed in Danish newspaper Politiken with my colleague Saila Stausholm. I reproduce it below, liberally translated, for those interested. Given the op-ed format, it naturally has certain limitations and a certain style that differs from my usual writings on this blog – so take that into account. Here we go: The Paradise…

-

Book review: Global Tax Governance – What is wrong with it and how to fix it

One of the major 21st century challenges for politicians and polities at both the national, regional and international levels is the governance of ever-more global, mobile and flexible economic and financial flows. No more so than in the area of taxation, which looks likely to remain the last bastion of entrenched perceptions of national sovereignty, an undisputed cornerstone…

-

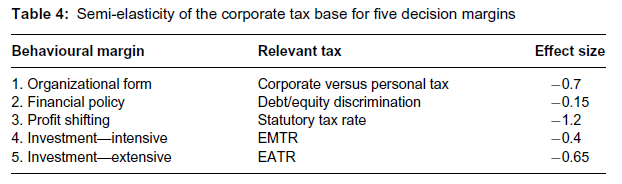

We’re changing the equation of tax competition and corporate profit shifting

Within tax economics, one of the central arguments for tax competition and low(er) taxes on capital, including corporate profits, is that it leads to increased investment and growth (at least in some countries, mostly small open economies). Why? In short, we know that corporate tax rates and rate changes have behavioural effects. Capital income may…

-

Catching Capital: Thoughts on Dietsch and tax competition

Globalisation and the intensified competition among firms in the global marketplace has had and continues to have many positive effects. However, the fact that tax competition may lead to the proliferation of harmful tax practices and the adverse consequences that result, as discussed here, shows that governments must take measures, including intensifying their international co-operation, to protect their tax bases…

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.