-

The new political economy and geography of global tax information exchange

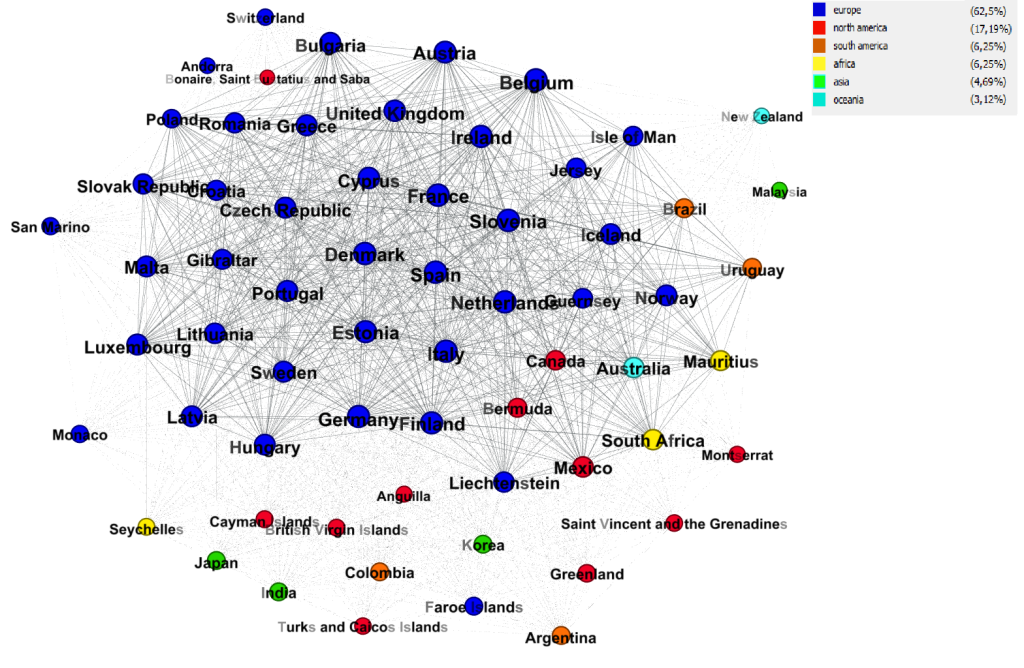

The OECD has recently released information on the two most important recent global networks of global tax information exchange. They are, respectively, the networks of exchange of country-by-country reporting (CBCR) and exchange of financial account information (through the Common Reporting Standard, CRS). These networks give a unique look into the new political economy and geography of…

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.