-

The EU ‘no taxation’ thesis, no more?

-

The new political economy and geography of global tax information exchange

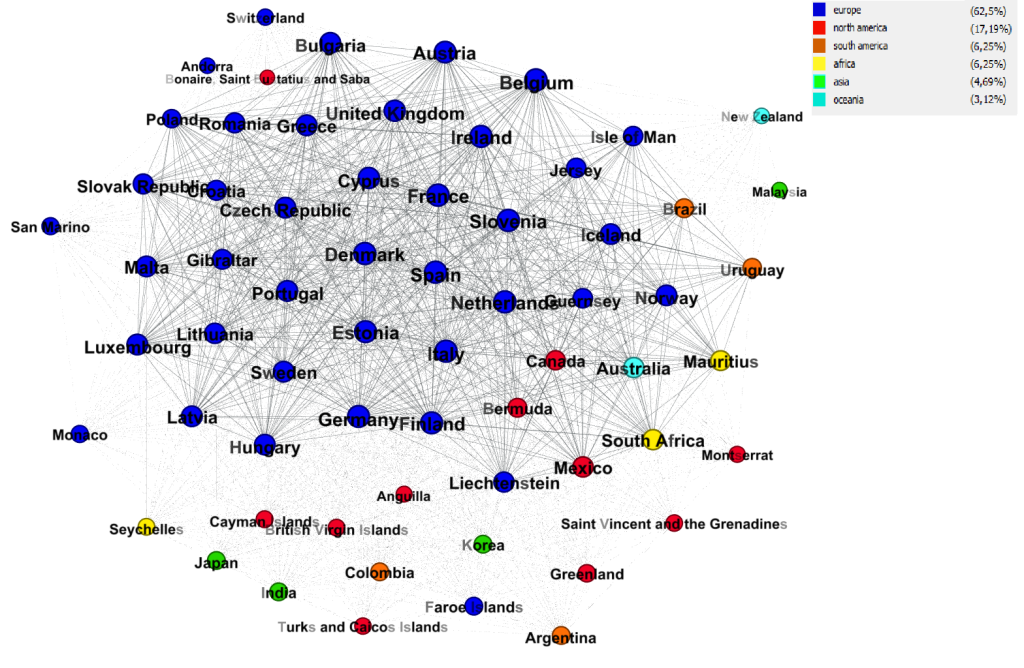

The OECD has recently released information on the two most important recent global networks of global tax information exchange. They are, respectively, the networks of exchange of country-by-country reporting (CBCR) and exchange of financial account information (through the Common Reporting Standard, CRS). These networks give a unique look into the new political economy and geography of…

-

Five years of EU tax policy recommendations: Key trends in European taxation

The European Union is a major player in international tax politics. Alongside the OECD, the EU has arguably been the most significant actor in redesigning international as well as national tax rules and norms over the past decade. So it matters what the EU’s institutions and its Member States are doing and saying on tax…

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.