-

The Show Must Go On

-

The new political economy and geography of global tax information exchange

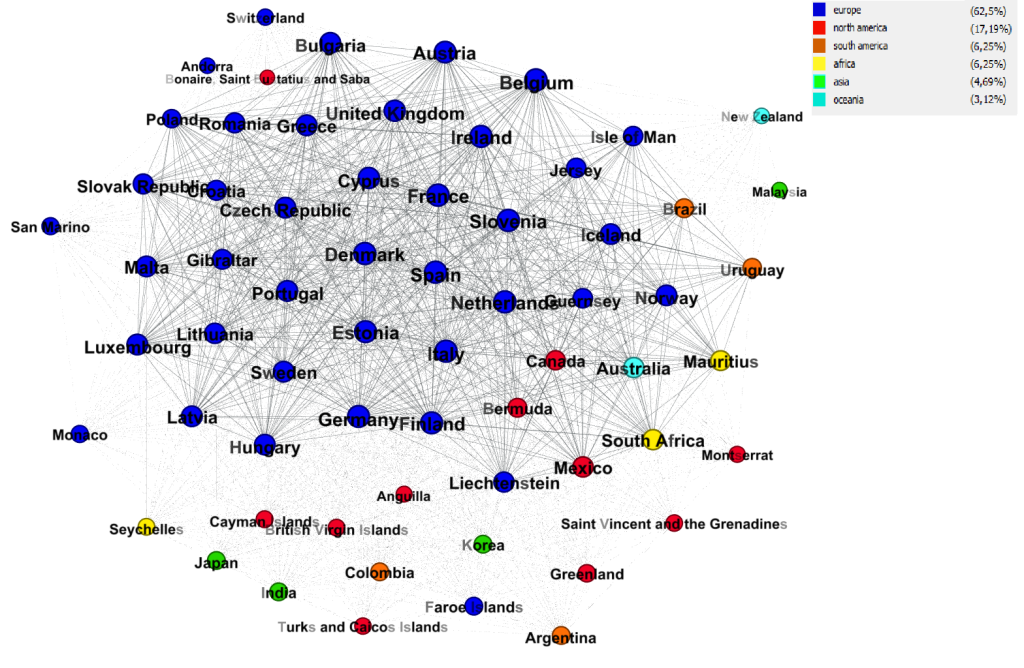

The OECD has recently released information on the two most important recent global networks of global tax information exchange. They are, respectively, the networks of exchange of country-by-country reporting (CBCR) and exchange of financial account information (through the Common Reporting Standard, CRS). These networks give a unique look into the new political economy and geography of…

-

The quiet BEPS revolution: Moving away from the separate entity principle

For the longest time, international law has treated multinational enterprises (MNEs) as consisting of separate, independent units, rooted in separate national jurisdictions. Apple’s US corporate headquarters is distinct from its Irish holding company, which is distinct from its local national subsidiaries – even though they are all part of the same multinational group. Their reporting compliance and tax liabilities are,…

-

Subscribe

Subscribed

Already have a WordPress.com account? Log in now.