For the longest time, international law has treated multinational enterprises (MNEs) as consisting of separate, independent units, rooted in separate national jurisdictions. Apple’s US corporate headquarters is distinct from its Irish holding company, which is distinct from its local national subsidiaries – even though they are all part of the same multinational group. Their reporting compliance and tax liabilities are, to a large extent, manifested separately at the country-level.

This ‘separate entity’ principle resonates throughout international taxation. It is, in particular, the basis of the entrenched arm’s length standard (ALS), the notion that related-party trade should accord to market terms.

The OECD/G2o BEPS (Base Erosion and Profit Shifting) project is, however, fundamentally challenging the separate entity principle. Stronger CFC (controlled foreign corporation) rules (Action 3) will manufacture formal links between group entities located in high-tax and low-tax jurisdictions. Tightened interest deduction rules (Action 4) will mandate group-wide formulas for thin capitalisation. Expanded use of the profit split method in transfer pricing (Actions 8-10) will put pressure on the ALS. And new transfer pricing documentation and country-by-country reporting (CBCR) obligations (Action 13) will provide tax authorities with more and better information on corporate group structures and value chains.

This trend is not a BEPS noveltyz Rather, the BEPS project underscores and accelerates a trend that has been emerging and increasing over the past 10-20 years in particular. There has been, and continues to be, a gradual move towards treating MNEs as unitary structures, rather than distinct fragments.

Interestingly, it is one of the more inauspicious regulatory innovations that provides the best illustration of the BEPS challenge to the separate entity principle: reporting mechanisms.

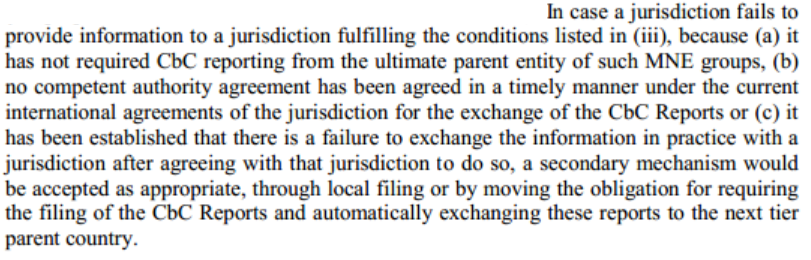

How can something so trivial be so crucial? Let’s take a step back first. Back in 2015, when the OECD, the G20 and a host of other stakeholders were discussing country-by-country reporting, one contested question was: How and where are companies going to submit their reports to tax authorities? Civil society groups wanted companies to file locally in all jurisdictions where they operate (e.g. to accommodate developing countries), while business lobbies advocated headquarter filing in the parent country of residence (to ensure more ‘trustworthy’ tax administrations would gatekeep the data). The eventual outcome was somewhat of a compromise. Parent-HQ filing was chosen as the primary filing mechanism, but the agreement also built in a secondary mechanism, a ‘safety valve’ of sorts. Thus, in the February 2015 recommendations on BEPS Action 13, the OECD introduced this:

And in the June 2015 Implementation Package, the secondary mechanism was detailed further. Here, we learnt that a subsidiary may be required to file the CBCR if:

a) the parent is not required to file in his home country, or

b) international information exchange or treaty sharing agreements are insufficient for the report to be exchanged from the parent company home country, or

c) there has been a “systemic failure” by the home country as regards the report.

In other words, if, for one of the stipulated reasons, a tax administration is not able to obtain the CBCR of an MNE with a subsidiary in its jurisdiction from another country’s tax administration, the tax administration in question can request the CBCR to be filed locally, by the subsidiary.

Make no mistake: This is groundbreaking. The UK HMRC and the Danish Skat can now force Apple’s local subsidiaries to obtain and provide extensive information on its global taxation and economic activity, in case they cannot procure that information from the US IRS due to a failure on the part of the US legislature, Apple, the IRS or the treaty system. And the same goes for developing country tax administrations.

But this is extraterritorial jurisdiction, surely? An espoused phenomenon in international law and international relations, a threat to the SOVEREIGNTY of nations. We are, after all, requiring purely local managers to provide information beyond the geographic boundaries of their authority, no? How would they even have access to that information?

Except, remember, we are moving towards treating MNEs as unified entities, not as disjointed networks. Therein consists the BEPS challenge to existing international law.

And this challenge is clearly on display. I want to highlight two ways in particular we can observe this:

Firstly, national law-makers are questioning whether it is even constitutional for them to enact or enforce this legislation. As EY note, in the context of the EU implementation of the BEPS agreement:

Certain Member States had expressed concerns that they may not be in position under their legal systems to require the full information of a given group from a subsidiary that cannot obtain or acquire all the information required for fulfilling the reporting requirement.

In the EU context, the proposed solution is to allow subsidiaries to file partial information (what they have available), while countries maintain the right to penalise non-compliance in such instances. But other countries have already implemented the BEPS regulation, which they may or may not be able to actually enforce, both practically and legally.

Secondly, and perhaps most blatantly, the secondary mechanism has led to panic among US multinationals. Why? While other countries have implemented the BEPS Action 13 requirements for financial years starting 1 Jan 2016, as agreed, the US has only required its companies to file for financial years starting 1 Jan 2017, to give an extended adjustment timeline. So there is a very real possibility that US multinationals, many of which have a lot of foreign subsidiaries, will be required to file locally for FY2016.

In response, the US has sought to allow voluntary filing of CBCR reports by US MNEs for FY2016. The proposed US regulations specify:

The Treasury Department and the IRS intend to allow ultimate parent entities of U.S. MNE groups and U.S. business entities designated by a U.S. territory ultimate parent entity to file CbCRs for reporting periods that begin on or after January 1, 2016, but before the applicability date of the final regulations, under a procedure to be provided in separate, forthcoming guidance.

The US is not alone, though. Recent OECD guidance on voluntary filing notes that also Japan and Singapore face similar issues.

The fact that OECD felt the need to issue guidance on such an otherwise trivial topic, and that American, Japanese and Singaporean MNEs are pushing for voluntary filing, underlines the dilemma created by secondary filing. There would be no push for voluntary filing if the secondary mechanism wasn’t seriously threatening existing standards within international law. Increased compliance burdens from expanded reporting requirements was the main criticism of multinationals in response to BEPS Action 13. So it should make us pause that they are now mobilising to voluntarily report to the IRS above and beyond their legal obligations.

But the secondary filing mechanism is just one or many streams pushing for a change in the perception and legal treatment of MNE groups. The ultimate push in this direction is, of course, unitary taxation, which would allocate tax based on the total consolidated worldwide income of MNEs.

What all these developments have in common is that they point in one direction: Increasingly, we will likely see legislation adjust to the new “reality”, that multinationals are not loosely connected collectives but rather more closely integrated enterprises.